Russia’s economy seems to be being doing a lot better than was expected. The International Monetary Fund (IMF) recently revised its forecast for this year’s contraction up from -8% to -6% and the Central Bank of Russia (CBR) is even more optimistic, having revised its forecast for this year’s contraction to a mild -5%.

These revisions come on the back of a slew of other surprises that have led many to say sanctions are failing. Chief amongst these results is the ballooning current account that, instead of going negative, has exploded and Russia is currently earning more money from its energy exports than it has ever earned before – despite shock the economy received from the imposition of some of the most extreme sanctions ever imposed on any country.

The crisis induced by the invasion of Ukraine is now being likened to the relatively mild shock of 2015 oil price crisis or the impact of the pandemic in 2020 rather than one of the two historical crashes in 1998 or 2008.

Not so, says a paper released by Yale Chief Executive Leadership Institute (Yale CELI) in July, which claims the damage done to Russia is far worse than it seems and that in fact the economy has come to a standstill and that many of its main problems are “unsolvable.”

“Looking ahead, there is no path out of economic oblivion for Russia as long as the allied countries remain unified in maintaining and increasing sanctions pressure against Russia,” writes Jeff Sonnenfeld, the founder and CEO of Yale CEIL, who has become well known for the widely cited list of foreign companies exiting Russia his group started compiling shortly after the invasion.

The paper has caused some controversy, as it takes an extreme line at a time when there is still no consensus how effective the West’s sanctions have been. The Yale paper is at one end of the spectrum arguing Russia’s economy has been crushed, whereas at the other end pundits point to the huge amounts of cash flowing into Russia’s coffers and the significant sanctions leakage caused by Russia’s partners in the rest of the world refusing to adopt the sanctions regime. There is plenty of evidence to support both sides of the argument.

“There’s a growing debate on just how much Western sanctions have hurt Russia’s economy. Some point to the strength of oil exports and the ruble as evidence that Russia has weathered the crisis well so far. Others, including a recent paper by academics at Yale University, conclude that “the economy is being crippled from all sides” due to the loss of Western technology. We think the reality lies somewhere in between,” says Liam Peach, an emerging market economist with Capital Economics. “The upshot is that Russia’s economy is in the midst of a deep contraction, but the (polarised) debate about how the economy is faring misses the point that there is a vast divergence between sectors.”

Sonnenfeld’s paper is a through and extensive expose of the vulnerabilities of the Russian economy, and correctly identifies many of its vulnerabilities. But it also contains many omissions, a selective use of examples, and some glaring factual errors.

It is written more as a polemic and as Yale CEIL is a business school, not an academic institution, this is not an academic peer-reviewed paper. Sonnenfeld is a specialist in management, CEO leadership and corporate governance, on which he is widely published, and a former professor at Harvard Business School.

The introduction to the paper promises evidence based on non-state statistics but delivers little on this front, and despite opening with a claim that official statistics are unreliable, it relies heavily on the official statistics throughout, raising eyebrows amongst professional economists that have reviewed the paper.

“I would also like the report to provide more of the "cross-channel checks" and "data mining through complex big data sources" as example of cross-check for official stats are hard to find in the text,” Alexander Isakov, formerly the chief economists at VTB and now head of Bloomberg’s economics team, said in a commentary on the paper.

It is also littered with assumptions of things that are “almost certainly” true, without backing up these assertions with forecasts or citing studies. The paper has as a starting point the standard Western take on “Putin’s Russia” as an oligarchic and kleptocratic petrostate that continues to be mired in a Soviet mentality that takes no account of the diversification of the economy over the last three decades, nor that it is by far the most prosperous of all the Former Warsaw Pact countries that didn’t join the EU.

“Another similarity underlying the modern Russian economy and the Soviet era economy – and which further highlights the structural weakness and lack of depth of the Russian economy – is the fact that extractive institutions persist,” Sonnenfeld writes.

Indeed, Sonnenfeld refers to “Soviet” 19 times in the paper, whereas Russian scholars and correspondents rarely reference the Soviet Union in writing about modern Russia other than in changes that have occurred “since the Soviet Union...”

Starting at the end, the paper draws six main conclusions:

Energy: Russia’s strategic positioning as a commodities exporter has irrevocably deteriorated, as it now deals from a position of weakness with the loss of its erstwhile main markets and faces steep challenges executing a “pivot to Asia” with non-fungible exports such as piped gas – as we explain further in Section II of this paper.

Import substitution: Despite some lingering leakiness, Russian imports have largely collapsed, and the country faces stark challenges securing crucial inputs, parts and technology from hesitant trade partners, leading to widespread supply shortages within its domestic economy – as we explain further in Section III of this paper.

Domestic production: Despite Putin’s delusions of self-sufficiency and import substitution, Russian domestic production has come to a complete standstill with no capacity to replace lost businesses, products and talent; the hollowing-out of Russia’s domestic innovation and production base has led to soaring prices and consumer angst – as we explain further in Section IV of this paper.

International companies: As a result of the business retreat, Russia has lost companies representing ~40% of its GDP, reversing nearly all of three decades’ worth of foreign investment and buttressing unprecedented simultaneous capital and population flight in a mass exodus of Russia’s economic base – as we explain further in Section V of this paper.

Budget problems: Putin is resorting to patently unsustainable, dramatic fiscal and monetary intervention to smooth over these structural economic weaknesses, which has already sent his government budget into deficit for the first time in years and drained his foreign reserves even with high energy prices – and Kremlin finances are in much, much more dire straits than conventionally understood – as we explain further in Section VI of this paper.

Financial markets: Russian domestic financial markets, as an indicator of both present conditions and future outlook, are the worst performing markets in the entire world this year despite strict capital controls, and have priced in sustained, persistent weakness within the economy with liquidity and credit contracting – in addition to Russia being substantively cut off from international financial markets, limiting its ability to tap into pools of capital needed for the revitalisation of its crippled economy – as we explain further in Section VII of this paper.

Sanctions effectiveness: Looking ahead, there is no path out of economic oblivion for Russia as long as the allied countries remain unified in maintaining and increasing sanctions pressure against Russia.

Despite the many problems with the Yale paper its main conclusion that the Russian economy has been deeply and irrevocably wounded is correct and the paper lays out the various challenges Russian President Vladimir Putin must face extremely clearly.

Where the debate starts is how well is Russia coping with the sanctions and what their long-term consequences will be. Sonnenberg is correct in highlighting the devastating impact of the technological sanctions on Russia, as there is little the Kremlin can do to replace Western equipment and software, and almost all sectors of the economy remain highly dependent on Western imports. Without these imports Russia’s overall growth potential has been reduced from the already low 2% per year – due to the Kremlin’s decision to divert its earnings from investment into building Putin’s Fiscal Fortress over the last decade – to 1.5% now, according to the Central Bank of Russia (CBR), or less.

But the Yale paper takes an extreme position on the impact of sanctions on the economy and leaps to several conclusions that are not justified, or at least remain highly debatable. Below bne IntelliNews runs through the issues raised by the conclusions above.

ENERGY

Oil: Russia’s position as a major commodity exporter has definitely been badly affected, but Yale argue that oil production will be reduced from the current 10.7mn barrels per day to 6mn bpd by the end of the decade – an extreme estimate that is shared by few analysts.

The government’s official forecast for oil production is that it could fall to 9mn bpd this year from the 11mn bpd produced in the first two months of this year and it did fall in the first two months of the war as international oil traders shunned Russian oil. But since then sanction leakage to India, China, Kingdom of Saudi Arabia (KSA) and most recently Egypt, has seen exports recover and production rise again to 10.7mn bpd in June, at which level it is expected to stabilise.

Sergey Vakulenko, an oil analyst that has worked for leading Russian and international oil companies for decades, challenged this assumption directly in a recent podcast “How Russia Engineered the Perfect Gas Crisis” and says that while oil production will be curtailed somewhat, it will not fall dramatically. Even though the service companies like Schlumberger will leave the country, they will sell their Russian businesses to locals, all the equipment will remain and that 30% of their global staff are Russian speaking, already forming a large pool of experts to hire. The government’s own estimate is that oil production will slide 15% this year to around 9mn bpd and at the moment the sector is on target to do better than that.

Sonnenfeld also argues that Russia’s share in global energy market is small, whereas its share in budget revenues is large:

“The importance of commodity exports to Russia far exceeds the importance of Russian commodity exports to the rest of the world.”

However, that is not how markets work. In 2021 there was never a large shortage of gas, just the fear that there would not be enough to get through the winter. But just by squeezing the flows as Gazprom tightened supplies by a fraction of the total deliveries was enough to drive prices up twenty-fold. Russia is a big enough player in the energy markets to wield significant market power, even if its total share in the market is small.

Creating a tight market means that Gazprom and the major oil companies are currently earning huge windfall profits. Nadia Kazakova, an analyst at the UK-based Renaissance Energy Advisors, told RFE/RL that based on current prices and volumes, she expects Gazprom to earn $79bn in European export revenue this year and $67bn next year, far surpassing the record $51bn it received in 2021. The same is true for the oil companies: reduced volumes are more than compensated for by higher prices.

The same is true for oil, where the small reduction in production from 11mn bpd to 10.7mn bpd is more than compensated for by the $100-plus price for a barrel of oil.

The ability to affect supplies at the margin and the huge effect that has on prices is also visible in the wheat markets, which are ruled by similar commodity market dynamics. Together Russia and Ukraine’s wheat trade accounts for a mere 0.9% of total global wheat production but 30% of the traded wheat business. In theory, global production has to rise by very little to cover the shortfall, but the gap in the traded supply caused by the war has sent wheat prices to all-time highs.

Geographical distribution must also be taken into account too in all these commodities. Europe and the US have sufficient wheat to meet their needs, but Africa is highly dependent on Russia and Ukraine. Likewise, Russian oil mostly goes to Europe, but it is possible to send it by ship to India and China, just that adds about $5 to the cost of a barrel. Europe’s supplies of oil come by pipeline and are essentially free.

This commodity price inflation is highly infectious: the US doesn’t import Russian wheat or oil but because both are globally traded commodities, if wheat and oil prices do spike, they will spike on the US domestic market too.

So far, Russia’s oil exports and production have weather the storm very well and even the 15% fall in production the Russian Ministry of Finance was predicting in March is unlikely to come to pass. After an initial fall in the first two months of the war due to self-sanctioning by oil traders, by June oil production started to rise again and was up 5% year on year to 10.7mn bpd compared with about 11mn bpd in January and February, as India, China and Kingdom of Saudi Arabia (KSA) took up most of the slack created in Europe. More recently, at the start of August it was reported that Egypt has now joined the club and is letting Russian oil ships dock, and reloading their cargoes on to other vessels for transport to the rest of the globe.

The Yale paper states the discount on Russia’s Urals blend to the benchmark Brent is $35 per barrel, which was the case during the initial shock. However, as Russia’s production and exports start flowing again that discount has already narrowed to $15, Kommersant reports, and is expected to narrow further as new transport routes are established, a fact Yale failed to note.

Leakage: Sanctions in general, and self-sanctions by companies of products not on the proscribed list, have led to a collapse of imports to Russia, which ironically has only improved Russia’s current account further. One of the basic flaws in the sanctions regime is that the oil and technological sanctions are working against each other: oil and gas sanctions drives up price and increases revenues, while the much more effective technological sanctions reduce imports and also drive up the current account surplus even further.

The problem is sanctions on commodities are very leaky. The recovery of the oil exports shows that the market is already adjusting and new trade routes are emerging as non-G7 countries step into the void left by Europe and the US.

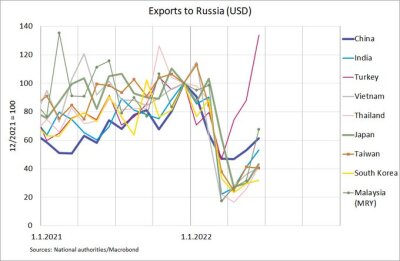

Exports tumbled after the sanctions regime was introduced and remain way down on pre-war levels, but by July they have already started to recovery. (chart).

While imports from most of Russia’s partners are still down by more than half – Germany -43%, France -69%, US -89% – those of Turkey in particular has soared and were up 46% y/y in June, as it steps into the role as Russia’s main conduit to the West. As bne IntelliNews reported, Turkey’s warehouses are packed full of goods on their way to Russia at the start of August. Turkish President Recep Tayyip Erdogan is testing the limits of the sanctions regime: how much can you export to Russia before bringing down sanctions on yourself.

China is playing a similar game, but has a lot more to lose than Turkey. It was already Russia’s biggest trade partner before the war and imports were down 60% y/y in June. The Yale report correctly highlights that China’s biggest trade partners are the EU and US, whereas Russia is only China’s eight most important export market. China cannot afford to get cut off from Western markets by sanctions and so its support for Russia is limited.

However, the relationship looks a little less asymmetrical in terms of the actual volumes of trade. China tends to run a balanced trade account, with all its partners exporting as many goods as it imports in dollar terms, as in the case with Russia. Moreover, it has already made some significant concessions after it threw its grain market open to Russian exports earlier this year – something Moscow has been lobbying for for years.

Nevertheless, Beijing remains ambivalent towards Moscow and has cut off all investment to the country since the start of the war. It remains to be seen just how this relationship will develop, as analysts are unanimous that China will pursue its own interests first and foremost.

Gas: On gas Sonnenfeld argues that the “Pivot to Asia” and the redirecting Russia’s gas pipeline infrastructure, which overwhelming goes west at the moment, to the east is an almost impossible task.

“As of 2021, a whopping 83% of Russian natural gas exports were received by Europe, although Europe has a far more diversified supply base, drawing 54% of its gas imports from non-Russian sources, including LNG from Norway, Qatar and Algeria in addition to significant domestic supply from sources such as the giant Groningen gas field in the Netherlands,” Yale writes. “Russia’s problems on the natural gas front, unlike Europe’s, are deeply ingrained in long-term challenges within its economic and political structure, not transitory in nature, and are ultimately unsolvable.”

This problem is not impossible to solve, as new infrastructure is already appearing. In 2021 Russia sent 155bn cubic metres of gas to Europe. Built in the 1970s, Russia’s gas pipeline infrastructure overwhelmingly goes west to Europe. The challenge, as Yale points out, is how to reorientate this infrastructure to the east. However, it’s not a question of “if”, but “when” – and now that Russia has definitively broken with the West the new question has become “how fast” this can be done.

Gazprom was always intending to pivot its business to Asia. Gazprom’s CEO Alexei Miller called Asia “Gazprom’s future” in a speech last autumn. It’s just the state-owned gas giant thought it had another decade to build the infrastructure. Now it has to do it as fast as possible at enormous expense, and without access to international financing to pay for the work.

The first leg of this pivot is already in place: the Power of Siberia 1 (POS1) gas pipeline came online in December 2019 and has a nameplate capacity of 38bcm that will be reached in 2024 and plans to increase it to 60 bcm – a third of what Russia send to Europe. Currently only 10 bcm is flowing this pipeline but those have already been rapidly expanding. The plan was to raise this over the next few years to 35 bcm as China develops its own domestic pipeline network in parallel.

Ground is expected to be broken on the extension, Power of Siberia 2 (POS2), next year or in 2024, which will have 50 bcm of capacity and will connect China directly to the massive Yamal gas fields in the Arctic. The construction is anticipated to take at least five years to complete.

The decision has also been made to build a long discussed route from Western Siberia via Mongolia to China for the Soyuz/Vostok gas pipeline, also with a capacity of 50 bcm, that will also break ground in 2024, as bne IntelliNews reported, and should be online by 2030.

Between them these three pipelines will be able to carry all the gas that is currently going to Europe into Asia sometime in the next 5-10 years, taking up all the slack created by closing down the European gas business.

Far from being an unsolvable problem, the pivot-to-Asia problem has already been solved. One of the pipelines is already built and the other two start construction in the next year. The remaining issues are simple a question of money and time.

Of course, building the pipelines is only the beginning of the process (and even that will not be simple). Questions of funding and signing a reasonable offtake deal with the Chinese still need to be dealt with, and with the Russians over a barrel the Chinese are certain to take advantage of the situation. According to Renaissance Energy Advisors’ Kazakova, China is currently paying a quarter of the price that Europe pays for gas.

As part of Putin’s calculation in deciding to invade Ukraine, he must have known of the high costs involved and clearly this is a cost he is prepared to pay. To understand Putin’s calculus: he puts Russia’s security well ahead of profits and prosperity – and that is one of the few Soviet things about him.

Copper: Missing major projects that will affect a sector’s development came up in the short section on copper too. This was included, as the metal is widely known as “Dr Copper”, as developments in the copper sector are believed to be indicative of long-term trends.

“Russia is not central to the copper value chain – and copper has never represented a meaningful proportion of Russia’s revenue from energy exports. Not only does Russia not possess any significant share of global copper reserves, but what reserves it does possess are already under-tapped and operating under-potential as is. This is unlikely to change, even if prices were to rise, as many expect,” Yale wrote.

The paper goes on to say that according to the US Geological Survey (USGS), Russian copper reserves are estimated to be only 7% of global reserves. Mine production, which generally aligns with the size of reserves, places Russia in eighth place with about 4% of global mine production, meaning that Russia’s already minor share of global reserves is dramatically under-tapped.

Yale has completely missed the Udokan copper mine that came online two years ago and is based on one of the largest copper deposits in the world. Far from being a minnow in the world copper market, Russia is about to become a powerhouse as production is ramped up to full capacity over the next years. Executives at the Udokan copper mine, a $3bn investment, told bne IntelliNews that ground has been broken on the deposit and the first copper produced. The enterprise will produce 135-137,000 tonnes of pure copper – in copper cathodes (50%) and sulphide concentrate (50%). The company forecasts that its output will increase by at least 30% in the next year and the expected life of the deposit is 50-60 years.

Like Russia’s place in the oil, gas and grain markets as well is the hold that Norilsk Nickel and RusAl have over the nickel, palladium and aluminium markets – metallurgy is ignored by the paper completely – Udokan will add another element to Russia's already formidable raw materials arsenal. As bne IntelliNews reported, Russian metals are deeply embedded in the global metals market.

MACRO & IMPORT SUBSTITUTION

The Yale paper is highly dismissive of Russia’s “delusional” attempts at import substitution but is correct that Russia’s various attempts at autarky have born little fruit so far.

Now faced with no choice, Russia will have to do the best it can. Thanks to sanctions the economic conditions have changed and there is no choice but to create domestic alternatives to Western technology or find alternative suppliers.

And this will take time. It is probably the biggest challenge the Kremlin faces, as bne IntelliNews detailed in a feature describing how the lack of precision tools is Russia sanctions soft underbelly, in July 2021. Since the fall of the Soviet Union, Russia has missed out on two revolutions in tool making and many more in electronics. It is not in a position to catch up in even the medium term.

Back in March CBR governor Elvia Nabiullina ominously warned industry that it would have trade down “at least two generations” of technology to be able to function, which will hurt productivity and permanently reduces Russia’s growth potential.

Even Russia’s agricultural sector will be heavily dependent on imports of inputs. For example, Russia is self-sufficient in potatoes, but the potato seeds are almost all imported.

“Nearly 90% of potato seeds in, Russia, for example, are imported, along with about 70% of rape seeds, and from 30 to 90% of fruit and berry crop seeds. Russia is self-sufficient only in wheat,” Carnegie fellow Alexandra Propkopenko said in a tweet.

This dependency can be overcome by sourcing the seeds locally, and many technologies will be recreated by reverse engineering or simply buying tech from India and China. But there is no denying that this is the most serious problem Putin faces from his break with the West. Yale claims that it is so bad that

“Despite Putin’s delusions of self-sufficiency and import substitution, Russian domestic production has come to a complete standstill with no capacity to replace lost businesses, products and talent,” Yale writes.

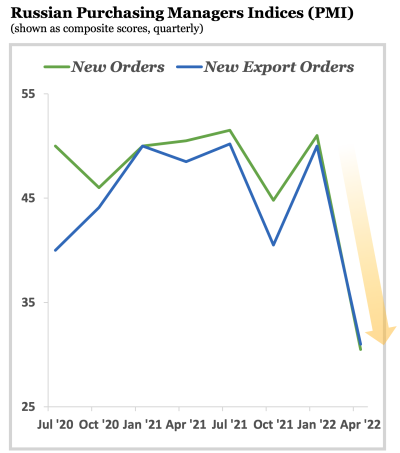

PMI: This is clearly an exaggeration, as Russia’s domestic production has not come to a “complete standstill,” a fact even illustrated by the data Yale includes in its own report. The car sector has come to a standstill, but that is the outlier, not the rule.

To illustrate the point Yale posted a chart showing the collapse of the S&P manufacturers PMI index that shows a very sharp fall since the war started.

However, this chart only shows the data up until April this year, whereas the June data was available at the time the report was released and other charts in the report have June data.

It appears that Yale deliberately ignored the more recent data, which paints a very different story: instead of collapse, the more recent PMI index shows a sharp recovery and indeed, in the July data (and not available to Yale for this report), the service PMI index shows strong growth. Far from coming to a standstill, the PMI index Yale used as evidence of a standstill actually shows strong growth in June and July.

Note, too, that this data is produced by the international credit agency S&P, based on more than a 1,000 interview with Russian managers on its panel. It is entirely independent of the government and cannot be manipulated, except by the selective use of the time series chosen by Yale.

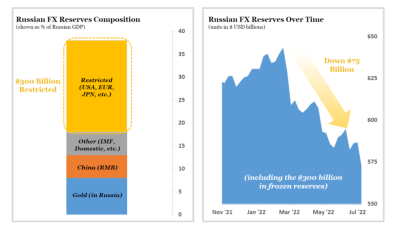

Gross international reserves: This is not the only place in the report where charts have been used to paint a blacker than real picture of Russia’s economic performance. Another chart shows the decline in the CBR’s reserves under the title “Russian FX Reserves Bleeding Out Fast.”

This chart is based on CBR numbers and shows that Russia’s reserves have fallen from its all-time peak of about $620bn at the end of January to the current $571bn as of July 29, according to the CBR, and by $75bn since the war started.

However, this is misleading, as while the CBR itself values its reserves in dollars, as Yale itself points out, most of its reserves are actually held in other currencies such as pounds, euros and yuan as well as around $140bn as physical gold. Indeed, the CBR went out of its way to de-dollarise its reserves, which now account for only about 11% of the basket, of which 6.6% of the total are part of the CBR’s money frozen in the US. Last July the Russian Finance Ministry announced that the share of US dollars in the country's c.$140bn national wealth fund had been reduced to zero.

The dollar has been on a tear and has strengthened by 10% since the start of the year, which will decrease the value of the CBR’s reserves valuation in dollars by something on the order of $40bn-$50bn from just the FX and gold price dynamic effects.

“We're in a strong Dollar "super-cycle" that's due to solid growth in the US while the Eurozone slips into recession, dragged down by Russian aggression. Euro is going well below parity,” said Robin Brooks, the chief economist at IIF.

It is hard to be sure, as the CBR has not released any new information on its basket’s make-up and always releases it with a long lag anyway so as not to affect the FX markets.

Clearly the reserves have suffered, as the pound in particular has lost a lot of value and even the price of gold has come off steeply from its March-April highs, accounting for a c.$5bn fall in the reserves' valuation. Altogether a lot, if not most, of the fall in reserves chart can be accounted for by the dollar’s strength. But Yale doesn’t attempt a discussion of the FX effects on reserves and simply suggests with its “bleeding out” label that the CBR has just spent this money – ignoring the fact that the financial sanctions prevent the CBR from spending any of its hard currency.

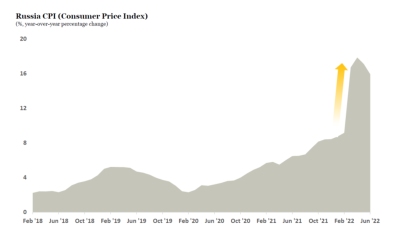

Inflation: Another problematic chart depicts inflation and was used to highlight the ropy state of the economy.

This time the chart’s data runs up until June, showing Yale had access to the current data. But what this section failed to do was to mention that not only do most countries in Emerging Europe have similar numbers but that Russia is the only country in Europe where inflation is now falling thanks to the fast action by the CBR – something perfectly obvious from the Yale chart.

Russian inflation peaked at 17.8% in April (chart) and is expected to fall further, which has allowed the CBR to cut rates four times since the emergency hike to 20% a few days after the war started. The CBR is also the only central bank in Russia that has reached the end of its tightening cycle and has been cutting rates. (chart). The situation with Russia’s monetary policy is made a lot more complicated by the capital controls in place, but none of this is mentioned or discussed in the report.

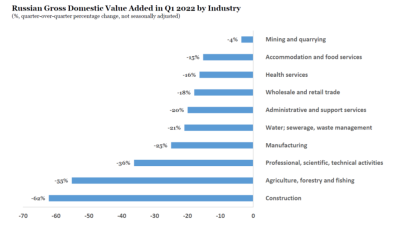

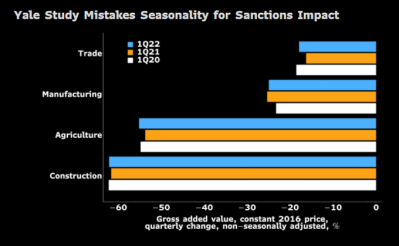

Sector growth: Domestic production quite clear has not come to a standstill – even according to the value added industrial production chart the report contains that shows many of the most important sectors baring a less than 20% decline, despite bearing the brunt of a huge economic shock. Moreover, Yale’s chart only shows the results for the first quarter and hence was affected by the first month of the war in March.

The second problem with this chart is that it is not seasonally adjusted, says Alexander Isakov, formerly the chief economist at VTB and now at Bloomberg. In that case the same chart shows that the economy actually grew compared to the first quarter results of previous years. (chart)

“The problem here is obvious: no seasonal adjustment. Each 1Q is weaker vs 4Q: long holidays, cold weather and harvest cycles: wheat doesn't grow in the snow,” said Isakov. “When seasonally adjusted, GDP actually expanded 0.5% in 1Q, before starting to drop in 2Q.”

It’s still not clear how each sector has been affected and industrial production numbers by sector is one of the statistics that RosStat is not publishing any more, but clearly some sectors are a lot more dependent on imported inputs than others. More information is needed.

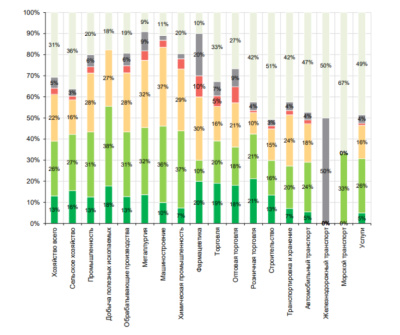

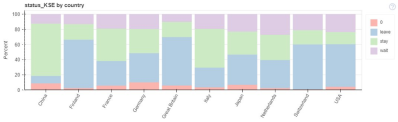

Companies are already beginning to cope with the new realities. CBR found in a separate survey (chart) that half of Russia's enterprises appear to have found new suppliers (end June), up from third in April. Only 3% say that replacement of Western supplies is impossible. Industries most exposed include pharma, chemicals, machine building, metals and mining, and processing.

Russian companies that do not rely on imports (light green)

Russian companies that are struggling to find alternative suppliers (orange)

Russian companies that find it impossible to get substitutes (red)

What is going on in industry is a very complicated topic, as it depends on what you look at. The Yale paper chose to selectively highlight the very worst affected sector – the car sector.

Almost wholly reliant on imported “just in time” parts, production really has come to a standstill, down by over 89% in June. As bne IntelliNews reported, production of car production has come to a screaming halt, as without the import of sophisticated parts, production has stopped in all of Russia’s biggest plants. Sales have fallen off 90% as well. (chart) But extrapolating this example to the whole economy doesn’t stand up.

Sector breakeven exchange rates: The Centre for Macroeconomic Analysis and Short-Term Forecasting (CMASTF) did an interesting study that sheds some more light on which sectors are the most vulnerable. It calculated what the exchange rate has to be for a sector to start losing money. At the time of writing the ruble-dollar exchange rate was RUB60 to the dollar.

It found in the “red zone” the most vulnerable sectors include crude oil, natural gas and other minerals (especially phosphates, diamonds, clay), which would incur heavy losses if the ruble strengthened to RUB45 to the dollar, as they around 80% dependent on exports. The wood processing and wood products industry has a break-even rate of RUB53, and railway rolling stock, aircraft and spacecraft of RUB61.

In the “orange zone” are things like coking coal and oil refined products, metallurgy, coal mining, food industry and furniture production and these have a break-even rate in the range of RUB30 to RUB40 to the dollar.

In the “green zone” are the chemical industry, electrical equipment manufacturing, crop and livestock production, which have break-even rates of below RUB16-RUB28. The most exchange rate insensitive industries are extraction of metal ores, the production of clothing, tobacco products and paper, as well as fisheries and fish farming, which have break-even rates below RUB16 per dollar.

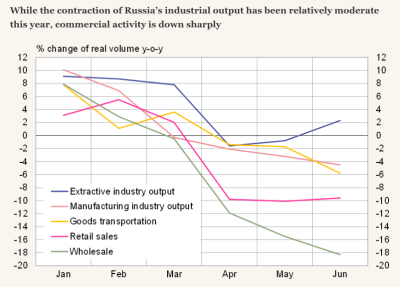

“There are still large differences in the tracks of various sectors of the economy. After declining last spring, extractive industry output rose in June, which largely came from the April drop in oil output and its accelerated June recovery. Services supporting extractive industries enjoyed continuous considerable growth,” the Bank of Finland institute for Emerging Economies (BOFIT) said in its weekly update.

Industrial production: Mining of metal ore in June was only 4% lower than it was in December. Manufacturing of basic metals was down by 10% and production of rolled iron was 20% lower. Production of natural gas slumped 23% y/y in June, but this is likely to reflect retaliation against the EU more than the direct impact of sanctions.

Russia’s oil sector, which is by far the most important in terms of GDP, exports and tax receipts, has held up well. Oil production has rebounded since April and in June was 1-2% lower than at the end of last year.

Despite a notable recovery in petroleum products, manufacturing output continued to decline in June, falling by 4.5% y/y. Most of the y/y drop in manufacturing output also in June resulted from the collapse of domestic car production, but significant declines in recent months in metal production and fabrication of metal products, as well as the chemical industry, have also had tangible impacts, according to BOFIT.

Construction activity, which has diminished since April, slid down in June to the same level it had been a year earlier. The slide in goods transport became steeper in June, falling by nearly 6% y/y. The sharp drop in wholesale activity began to level off, but wholesale volumes were still down by a whopping 18% y/y in June.

Household consumption has decreased sharply. Second-quarter household spending on goods and services was down by 7.5% y/y in real terms. Seasonally adjusted figures show that the volume of retail sales remained unchanged in June, but the sales were down by about 10% y/y.

While all these falls are serious and painful, they are not catastrophic and nowhere at a standstill. Like other observers, BOFIT puts this crisis on par with other major crises but not as severe as the two really destructive ones of 1998 and 2008.

“Household disposable income fell by just 0.8% y/y in the second quarter, although real wages were off by 5-6%. Consumption was drawn down by rising savings in the second quarter. Households showed similar patterns during Russia’s recessions in 2015 and 2020,” BOFIT reports. (chart)

Sanction proof sectors: In contrast to looking at the car sector there is the example of Segezha, Russia’s leading paper and pulp business at the other end of the spectrum. The CMASTF exchange break-even study puts paper in the “green zone” and one of Russia’s major industries that will not be badly effected by sanctions.

As bne IntelliNews featured in a cover story on Russia’s Green Gold, Europe’s paper and pulp resources are tapped out as all the available forests are under cultivation. In the same way that copper is key to development of the EV sector, paper and packaging is booming thanks to the growth of e-commerce and it is Russia that has the endless forests. Canada also has the same big forests, but because paper is heavy, the paper business tends to remain regional: Canada serves the giant US market; Scandinavia serves Europe, but has no capacity to expand production; and Russia serves Europe and Asia. Segezha IPO’d last April and has already put most of its production units in place.

How easily can Russia re-engineer to replace the Western inputs? To what extent Russia can replace imports remains an open question, but the reason that so many Russian sectors rely on Western imports is well illustrated by the cheese saga.

In 2014 in a tit-for-tat sanction, the Kremlin banned the import of all European agricultural products including cheese, which instantly disappeared from the shelves. Up until those sanctions, setting up a domestic cheese industry made little sense, as imports were cheaper and of better quality, but once there was no choice, the investments were made, and a domestic cheese industry appeared within about two years. Russian cheese is not as good as the French version, of course, but a wide selection of cheeses became available and Russian investors have poured money into the sector.

Another solution is laws allowing for “parallel imports” that were passed almost as soon as the war started. Western products can now be imported via “friendly countries” without their owner’s permission, after suspending the need to respect international intellectual property rights.

The bne IntelliNews correspondent in Moscow reports that many of products belonging to the international brands that have pulled out of Russia are already back on the shelves, including on Russia’s big e-commerce sites such as Ozon and Wildberries, but they all cost at least 20% more. Turkey is clearly intending to make a big business out of Russia’s parallel imports.

INTERNATIONAL COMPANIES EXIT

Yale is on its home turf when talking about the exit of international companies, based on its extensive and widely quoted list of companies that have departed. The report estimates that the leading 1,000 international companies that have said they may pull out represent 40% of GDP and their departure will

“reverse nearly all of three decades’ worth of foreign investment and buttressing unprecedented simultaneous capital and population flight in a mass exodus of Russia’s economic base,” says Yale.

However, this is clearly an exaggeration. While the combined turnover of these companies may be equivalent to 40% of GDP, this money will not disappear if these companies exit. The spending will simply switch to equivalent products, although the quality and choice will go down and many of these businesses will be sold to Russian companies in similar businesses.

The vast majority of these international companies are in the retail space. The investments they have made has not been into production, but into stores, marketing and advertising to build up their brands. Their departure will not affect Russia’s productivity but will affect the quality of life. And Russian firms are ready to step into their shoes as soon as they leave. Almost as soon as McDonald's pulled out, a new Russian firm called Vkusna I Tochka (Tasty, Period) took over its network offering exactly the same fare. For the economy there is no change in revenue or investment as a result of the hand over, but McDonald's had to book millions of dollars in losses.

It is also not clear which companies are leaving for good and which will remain. While over a thousand have announced their intention to leave the market, the number that have actually completed the paperwork are far fewer. Also, the decision to leave varies widely by the country of origin, according to another survey by the Kyiv Economic School that showed few Chinese companies are leaving, while few US companies are staying. (chart)

The departure of companies that have invested into production and supply key equipment, like Siemens in engineering, is a much more serious problem. Siemens single-handedly supplies almost all Russia turbines and most of its sophisticated train technology.

All in all, Russia has never attracted much FDI and the largest part of FDI that it does record is simply the profits of the international companies working in Russia reinvesting their profits into expanding their networks. Russia has always had so much cash that it has preferred to buy in equipment and expertise rather than rely on foreign investment for its progress. Foreign companies invested in Russia are going to be big losers and ironically the US is by far the biggest foreign direct investor into Russia.

The departure of the international brands will have a more serious impact on labour, as collectively these companies employ about 10% of Russia’s workforce. Currently most of these companies have simply suspended their operations but are still paying their staff. If they do exit and close their stores, millions could lose their jobs.

For the meantime, unemployment is at an all-time record low of 3.9% for both May and June (chart) and in the latest PMI results S&P panel of managers’ report that they have increased the number of workers they are hiring thanks to strong domestic demand. This might change in the autumn when the current emergency arrangements end. Foreign owners are looking to sell to local buyers and the government can be anticipated to come to rescue in significant cases. When Renault Nissan exited the giant AvtoVaz car plant in Tolgiatti, a mono-town where the local economy is entirely dependent on jobs at the factory, the Kremlin bought back the controlling package of shares for a reported one ruble. Extremely sensitive to its need to support the labour market, the Kremlin won’t let any really large foreign employer leave without finding some sort of new owner.

BUDGET

“Putin is resorting to patently unsustainable, dramatic fiscal and monetary intervention to smooth over these structural economic weaknesses, which has already sent his government budget into deficit for the first time in years and drained his foreign reserves even with high energy prices – and Kremlin finances are in much, much more dire straits than conventionally understood – as we explain further in Section VI of this paper,” Yale wrote.

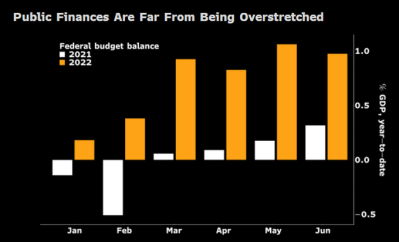

Yale appears to have spent very little time researching the section on government finances. First, the budget is not in deficit but was in surplus of 1% of GDP already in March and was still in surplus in June at RUB840bn ($14.4bn), or around 0.5% of GDP, thanks to the high oil revenues.

Bloomberg economist Isakov says that the claim the budget is in deficit is “hard to justify,” and an expected full year deficit of 2% GDP “does not endanger fiscal stability with manageable 20% debt/GDP.” Russia’s federal finances are not weak; they are strong. (chart).

“I think they’ll be nearly balanced at this pace. Maybe a small deficit of 1% is GDP. They have still large cash balances at MinFin they can use and banks’ liquidity is now up to over RUB2 trillion again. So plenty to cover borrowing if needed,” Elina Ribakova, deputy chief economists at IIF, said to bne IntelliNews.

Nominal revenues to the federal budget were up by 35% y/y in the first quarter and were still up by 17% y/y in March. Due to the spike in inflation, however, revenues were down in real terms in March as consumer prices rose by over 17% y/y, but since then, after inflation fell to 15.9%, real revenues are back in the black or at least flat by June.

Oil and gas revenues were hit by the reduced volumes being exported in June and July and will be reduced over the rest of the year, which is the source of Yale’s pessimism, but much of that is due to Gazprom’s decision to reduced flows of gas to Europe by 60% in June. And revenues could take a much bigger hit after December 5, when the EU is due to ban imports of Russian crude completely, followed by a ban on refined products on February 5 next year. How bad this will be remains unclear, but it will certainly reduce Russia's budget revenues noticeably.

“Russian oil & gas revenues collapsed in July, according to [Russia’s Ministry of Finance],” tweeted Carnegie’s Alexandra Prokopenko. “Failing of gas income is especially impressive, because of the energy war with the EU. Export duty fell 1/3: -32.9% y/y (64.9% y/y in June). We will see the reverse in o&g revenues during next month.”

Yale also overestimates the importance of oil to the budget, which made up 40% of revenues in March and prior to the war was often below 25% in a month thanks to the growth and diversification of the revenues (especially from VAT).

Prime Minister Mikhail Mishustin carried out a highly successful tax revolution when he was running the tax service that saw the tax take rise by 20% at a time when the tax burden rose by only 2% – mostly from collecting more taxes from the non-extractive sectors of the economy and stamping out the scams. However, the rise in oil prices this year has increased the share of oil revenues in the tax take.

Nevertheless, Russia’s budget is expected to record a mild deficit of RUB1.6 trillion (about 1% of GDP) by the end of this year – a level that it can easily cover with the funds in the National Welfare Fund (NWF) and issuing bonds to the banking sector.

"In general, we have a budget surplus, a conditional surplus, because all spending will go towards Q4, when we have to use all resources," Russian Finance Minister Anton Siluanov said during St Petersburg International Economic Forum (SPIEF) in June.

Secondly, Putin is not resorting to “patently unsustainable dramatic fiscal and monetary intervention” to paper over the cracks. Siluanov said in April that for the time being additional budgetary support this year will be of the order of roughly 2% of GDP – a modest figure. This is less than the 3% of GDP that Russian spent on social support in 2020 during the worst of the pandemic. And that was considered to be very modest, compared with up to 15% of GDP Australia spent on COVID support or even the 8.8% of GDP the US spent, according to the IMF. Most Western European countries spent more than Russia on social support in 2021.

According to Siluanov, the figure includes supplementary budget spending, investments in the economy funded from the National Welfare Fund and postponed corporate profit tax payments. Putin has also proposed granting a one-year postponement of the mandatory social contributions of employers for firms operating in most branches of industry and ordered a 10% increase in pensions and minimum wages in May.

Yale correctly states that Russia is now cut off from the international capital markets, but Russia’s access to them was already stymied in 2014 and the Ministry of Finance has never relied on the international capital markets for funds. Russia has been issuing a mere $3bn a year of Eurobonds since 2014 – a drop in the bucket – mainly as a benchmarking exercise for its corporate borrowers.

“Russia can continue to issue its version of domestic bonds, known as OFZs, but the total capital pool available within Russia domestically is a fraction of the financing needed to sustain these levels of spending by the Russian government over an entire economic cycle,” writes Yale.

This is wrong in that the pool of liquidity in the banking sector can cover the OFZ issuances and even before the war banks were buying around 75% of all the OFZ issued. Bloomberg economist Isakov reports that while bond issues were suspended in March, they have since resumed and by July the auctions had already reached “average 2021 levels” for the month.

Russian banks had been buying all the OFZ at auction when tensions flared. Foreign investors' share of the OFZ market rose to a peak of 34% last year but reduced to 20% as tensions built after the end of October of that year. Russia’s ability to attract foreign capital will be curbed now, but that will not stop the Ministry of Finance from tapping the bond market and the massive current account surplus it is earning for funds it needs.

FINANCIAL MARKETS

The discussion of Russia’s capital markets in the Yale report is fairly pointless, as it is still far too early in this conflict to be able to draw any conclusions from investment dynamics into equities about Russia’s long-term appeal.

The military conflict is in a slow-moving artillery duel that will not be resolved for months and the economic war between the West and Russia is escalating and just the gas war that is developing is likely to last all winter. These are not conducive conditions for making equity investment decisions.

However, the basic point that Putin has effectively destroyed Russia’s investment case for as long as he remains alive, and that Russia is permanently cut off from Western capital markets, is valid. Over the last three decades about half, the capital in Russia’s stock market has been speculative Western money, which is one of the reasons why the market has been so volatile – usually the best or the worst performing market in the world, depending on the news flow in any given year.

What changed in 2021, as bne IntelliNews extensively reported, is that the market finally came of age as domestic retail investors poured into Russian and international shares after interest rates on bank deposits fell to post-Soviet lows. Those same retail investors have been burned once again by the government after the market crashed for the umpteenth time. Indeed, a group of retail investors have launched a class action against state-owned banking giant VTB in June to try to get some of their money back.

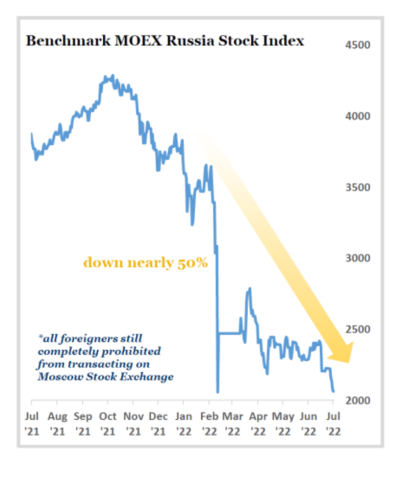

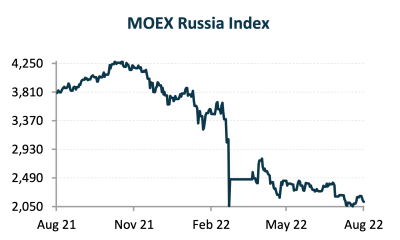

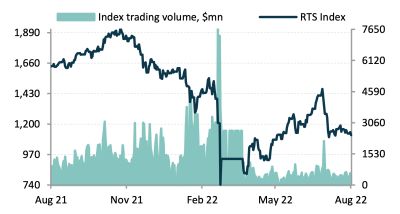

It is moot as to whether the market will ever recover. A chart of the ruble-denominated MOEX index in the Yale report shows the market in free fall, with the index down 44% YTD as of August 3, although a more recent chart shows the MOEX index flatter, albeit still sinking slowly ahead of the lifting of restrictions on foreign investors from “friendly” countries, allowing them to trade again from August 5; many are expected to sell their shares.

A chart of the dollar-denominated RTS shows the same thing: the RTS started to recover in the first two months, but has fallen 30% YTD since before the war and is now trading in a band around 1,100.

Drilling into the stocks grouped by sector and the picture is also more nuanced, with some sectors like chemicals (including fertilisers) actually making gains this year, but all the others have lost money, with metals and mining doing worst of all as of August 4.

Following the imposition of sanctions in 2014 after the annexation of Crimea the RTS traded in a band of 900-1,300 for about five years and the same is likely to happen this time – or for longer, as Russia can no longer be considered to be an open market economy, IIF’s Ribakova argued in a podcast with bne IntelliNews.

Yale’s chart again is employed to illustrate a dramatic crash, but stepping back and looking at the history of stock market crashes, while this one is bad it is not as bad as the previous worst cases.

The biggest crash came in August 1998, when the Asian currency crisis of 1997 spilled over into Russia. The RTS went from a peak of around 500 in the autumn of 1997 to fall to a low of 38 in October 1998. The market fell 85% in that year.

The next really big crash was in 2008, when the market fell from a peak of 2,400 in May that year to a low of 500, after funds were hit with margin calls that fuelled forced-selling and drove the market down beyond its natural floor of about 900. The full-year performance for that year was a fall of 72%.

Note that in both those crises the market bounced back very strongly the next year in terms of return on investment, even if the absolute values of the RTS index remained much lower for years afterwards.

This time the RTS has fallen from a peak of around 1,600 in October 2021 to a low of just under 1,000 in March, a fall of 46%. Since then, the RTS has recovered somewhat and at the time of writing was trading in a band around 1,100 with a YTD loss of 30%, which is better than the crisis induced by the oil price collapse in 2014.

However, there are two big differences with this crisis and all of the other stock market crashes. The first is that due to the CBR capital controls foreign investors were not allowed to sell their shares at all and they remained trapped in the market to this day. That also means the margin call mechanism could not operate – where investors are forced to sell their shares to raise cash to pay creditors compensation after a stock falls below a pre-agreed level.

Secondly, it is not clear if those investors will ever be allowed to sell their shares. And even if they are, it is not clear if investors will ever be allowed to buy Russian shares again due to sanctions. And on top of all that it is already clear that not many investors will want to buy Russian shares again after they have been through all of the above.

Russia’s equity market is currently de jure disconnected from the international market and probably de facto disconnected for a long time as well. In this respect the less than catastrophic collapse in share prices pales in comparison decoupling of Russia’s capital market from the international financial system. Russia’s stock market will be a domestic affair from here on in.

CONCLUSION

In conclusion the Yale report exaggerates the problems Russia’s economy is facing, but that its fundamental message is correct: the heavy sanctions imposed by the West are extreme and have fundamentally reduced its long-term growth potential.

The country will be permanently cut off Western technology that will cripple its productivity and Russia will be unable to develop this technology for itself for the foreseeable future, nor be able to buy it from anyone else.

It has also cut itself off from its most lucrative and closest markets. It will permanently lose its gas business with Europe and cannot develop a replacement market in Asia under five years at the earliest. Likewise, its oil business will be permanently reduced and less profitable. As a result of the change in orientation it has lost much of its price setting power and will have to sell energy to its remaining customers at deeply discounted prices.

These changes will reverberate to affect the budget eventually, as commodity prices return to normal levels and deficits will be harder to finance as foreign investors have been barred from Russia’s capital markets and are unlikely to return.

Putin’s plan seems to be to try to build a new market with the non-aligned countries of the Global South, but the reception there is only lukewarm, as most of these countries need to retain their good relations with the West in addition to wanting to buy cheap Russian commodities. Just how this balance will unfold will be the subject of bne IntelliNews’ reporting for the next decade.